Approaching or in retirement.

Betashield Portfolio Risk Management

Betashield is a risk management strategy intended to limit downside risk in your portfolio, allowing for more peace of mind during turbulent times in the market. Conversely, during periods of prolonged uptrends the portfolio allocation shifts to a more aggressive stance with the goal to better participate in growth.

Designed for investors who are:

Focusing on asset preservation.

Looking for a way to limit exposure to a catastrophic portfolio loss.

Searching for a reduction of losses to allow for quicker recovery.

Seeking to capture gains in long-term, up-trending markets.

Willing to accept a potentially lower return in exchange for risk reduction.

WHY IS LIMITING LOSS AN IMPORTANT GOAL?

The larger the loss in a investment scenario, the greater the subsequent recovery would need to be to break even.

The Method

The Betashield portfolio is designed for retirement-focused investors seeking asset preservation and protection against catastrophic portfolio loss. It aims to reduce losses, enable faster recovery, capture gains in up-trending markets, and lower risk in exchange for potentially lower returns.

During periods of prolonged uptrends the portfolio allocation shifts to a more aggressive stance with the goal to better participate in growth.

- Global Equity

- Opportunity

- Fundamental

- U.S. Equity

- International Equity

Global Equity

U.S. and Non-U.S.

Active Risk Management that seeks to avoid significant account value loss, with an underlying strategy seeking to maximize long-term capital appreciation in the global equity market.

Opportunity

Global

Active Risk Management that seeks to avoid significant account value loss, with an underlying strategy seeking to maximize long-term capital appreciation in the global equity market.

Fundamental

Global

Active Risk Management that seeks to avoid significant account value loss, with an underlying strategy to balance capital appreciation with preservation.

U.S. Equity

Active Risk Management that seeks to avoid significant account value loss, with an underlying strategy seeking to maximize long-term capital appreciation in the domestic equity market.

International Equity

Active Risk Management that seeks to avoid significant account value loss, with an underlying strategy seeking to maximize long-term capital appreciation in the international equity market.

Assets in a Betashield strategy will be incrementally shifted to a short-term government treasury ETF when market conditions deteriorate. As markets improve, the portfolios will gradually shift back to their original, more aggressive asset allocation in an effort to increase the growth potential of the portfolio.

When the negative market environment begins to unfold, the Betashield approach is intended to hedge the portfolio. If the negative market persists, the hedge can be increased in an attempt to mitigate losses.

SO WHAT HAPPENS WHEN

The Market Drops?

Upon the portfolio’s allocation to the hedge position, the Betashield approach will diligently observe market volatility and make necessary hedge adjustments. Based on a combination of performance and volatility, the algorithm will dynamically determine whether to augment or diminish the hedge, with the goal to strategically position the assets for enhanced growth potential.

Betashield risk management engages when portfolio performance declines in a neutral market.

The proprietary algorithm recalculates daily and signals defensive action.

Client accounts gradually shift into a hedge position using a short-term treasury ETF.

Treasuries are increased in 25% increments as performance and volatility decline.

This strategy aims to safeguard against fluctuating market behavior.

Treasuries can range from 0% to 100% based on market performance.

100% Invested

Base Portfolio

Neutral Asset Allocation

75% Hedged

Initial Market Decline

1st Hedge

50% Hedged

Further Market Decline

2nd Hedge

25% Hedged

Further Market Decline

3rd Hedge

100% Hedged

Further Market Decline

4th Hedge

SO WHAT HAPPENS WHEN

The Market Goes Up?

Once the portfolio has transferred funds to the hedge position, the Betashield approach will monitor market volatility and make necessary adjustments to the hedge. Depending on a combination of performance and volatility indicators, the algorithm will dynamically increase or decrease the hedge to position the assets for increased growth potential.

After moving funds to the hedge position, the Betashield approach monitors market volatility.

The hedge is adjusted based on a combination of performance and volatility.

The algorithm increases or reduces the hedge to position assets for increased growth potential.

If performance and volatility remain positive, funds are shifted back to the Base Portfolio.

Depending on portfolio performance and volatility, client accounts can be invested in the Base Portfolio at 0%, 25%, 50%, 75%, or 100%.

Shifting occurs in 25% increments.

100% Hedged

Fully Hedged

25% Invested

Initial Market Decline

1st Base Portfolio

50% Invested

Further Market Decline

2nd Base Portfolio

75% Invested

Further Market Decline

3rd Base Portfolio

100% Invested

Base Portfolio

Fully Invested

• Base Portfolio

• Hedged - Active Risk Management

STRATEGY

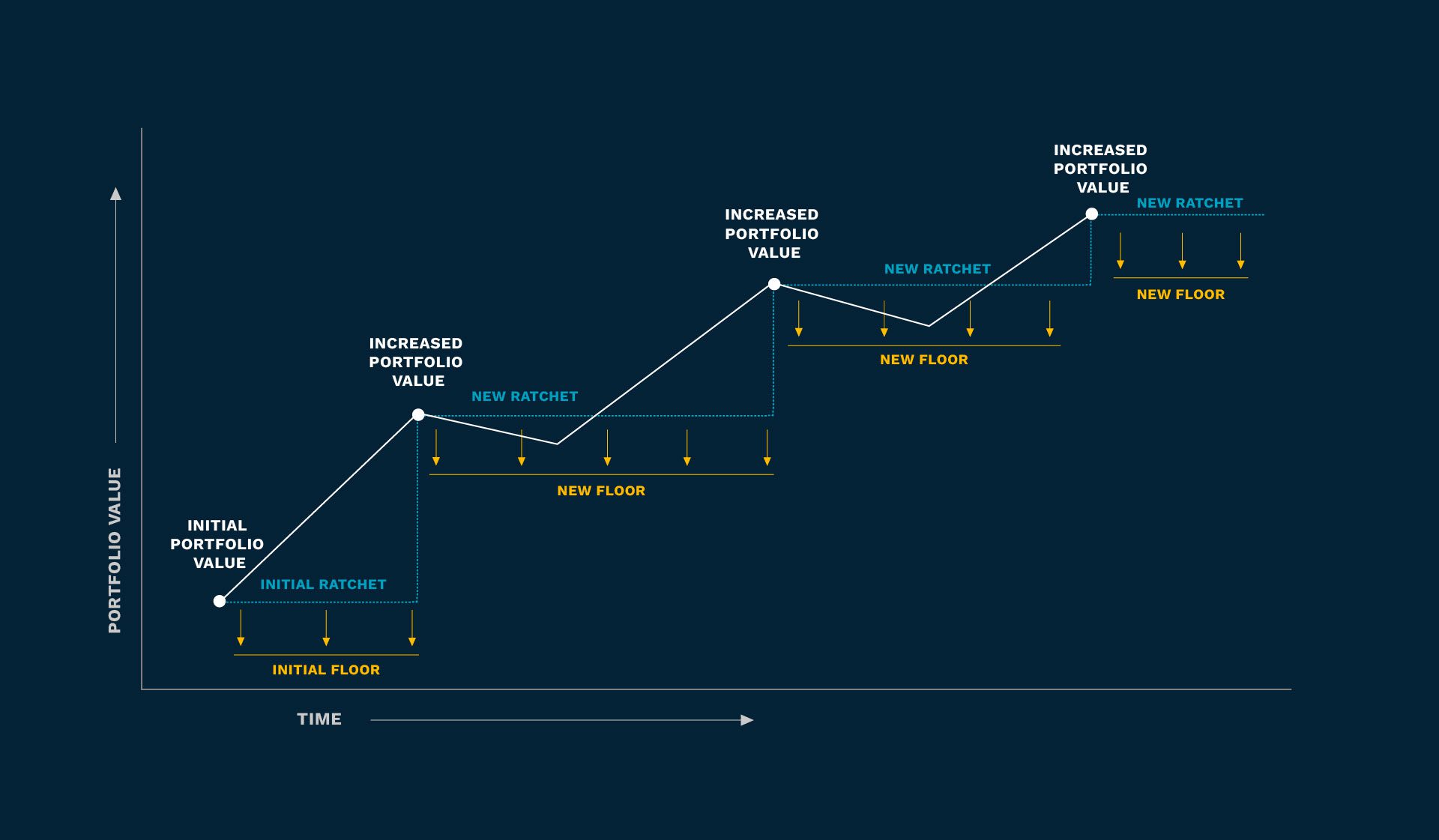

Establish a Floor

Ratchet UP

In an effort to limit the loss in a Betashield portfolio, our proprietary algorithm establishes a “floor” for each strategy. It is designed to act as a protective layer, monitoring investments based on targeted maximum loss percentages. The floor guides the proprietary algorithm but isn’t a guarantee. The strategy also adjusts the maximum allowable loss based on the portfolio’s highest achieved value, ensuring ongoing recalibration.

DISCLOSURES Investment advisory services provided by Alphastar Capital Management, LLC (“Alphastar”) as the investment adviser. This illustration is presented for informational purposes and is not an offer or solicitation for the sale or purchase of any security or other financial instrument or to adopt a particular investment strategy. All charts and graphs are shown for illustrative purposes only. Investors should consult their financial and tax professionals before implementing any strategy. Total fees and expenses, including advisor, platform, brokerage and custody fees for an account invested in a Betashield strategy will vary and yield different results. Consult our Form ADV Part 2Afor additional information about Betashield strategy fees and expenses and ask your advisor how these fees apply to your account. All analyses and information contained herein are based on sources believed to be reliable, including information received from third-party sources, but no representation or warranty of any kind, expressed or implied, is made including but not limited to any representation or warranty concerning accuracy, completeness, correctness, timeliness or appropriateness. The information contained herein is as of the date referenced above, and Alphastar does not undertake any obligation to update such information in any form or format. All investments involve the risk of potential investment losses as well as potential for investment gains. Past performance is not a guarantee or predictor of future results of any particular investment, benchmark or indices nor a guarantee of achieving overall financial objectives. Investments offering the potential for higher rates of return also involve a higher degree of risk. The risk algorithm (“Algorithm”) used in the Betashield portfolios is NOT A GUARANTEE against loss or declines in the value of a portfolio. While the algorithm was designed with the goal of limiting account drawdowns in declining markets, Alphastar is not able to predict market conditions or ensure that the Algorithm will limit drawdown as designed. Portfolios are subject to general market risk and risks related to economic conditions. The portfolios’ underlying investments fluctuate in price and may be sold at a price lower than the purchase price resulting in a loss of principal. TheBetashield portfolios have no principal guarantees, no guarantee that the account will grow, no guarantee the account will not lose value, could lose more than the stop-loss ranges of each portfolio based on extreme market conditions such as a “flash crash” or “back-to-back significant losses”, or “other unplanned economic, world, or negative event”, and do not have guaranteed lifetime income. During the time the funds are out of the stock market they will not participate in any stock market gains and the Betashield performance may be lower than market performance in markets with positive performance. It is understood that the underlying Betashield portfolio could be considered aggressive by itself, but a portfolio strategy which employs the risk management overlay, the assumed risk is lessened. The Betashield portfolio is not designed to act like the S&P;500 Index, nor the Dow, nor the NASDAQ, it is designed to decrease the volatility historically exhibited in those indexes. The technical goal of each Betashield portfolio is to potentially reduce portfolio standard deviation (risk) and potentially increase return opportunities as compared to risk(Alpha). Risk reduction and increased performance is not guaranteed. The underlying investments are neither FDIC-insured nor guaranteed by the U.S. Government. There may be economic times where all investments are unfavorable and decline in value. Please evaluate your clients’ circumstances and risk tolerance to understand if these investments are right for them. Clients may lose money.